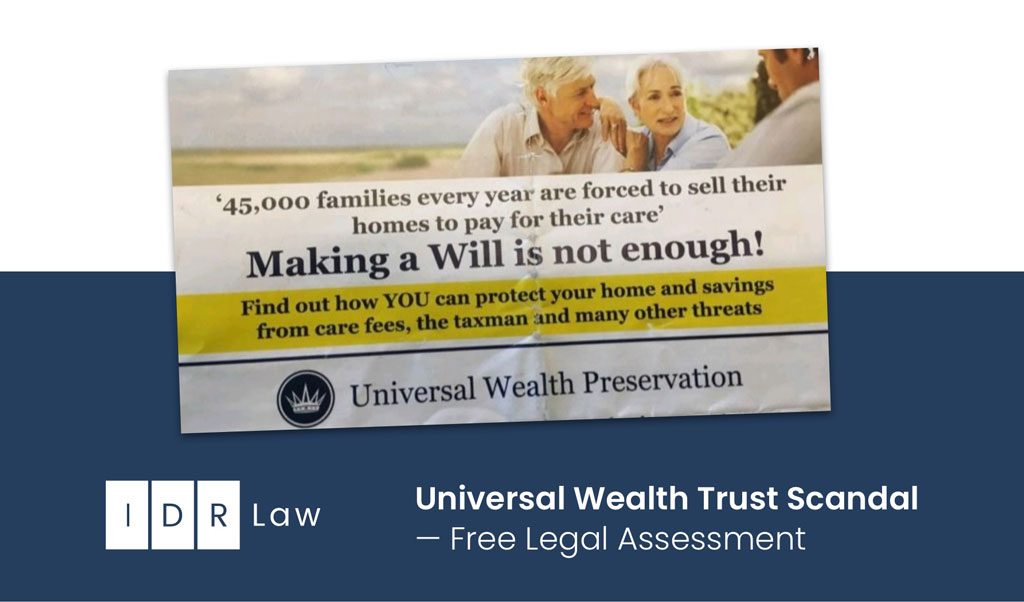

Keep it in the family and avoid care home fees

In 2012 our clients attended a seminar arranged by Universal Wealth on asset preservation trusts (“APT”). Our clients were interested in understanding if anything could be done to safeguard their son’s future inheritance and to avoid care home fees in the future.

The trusts

The seminar they attended proposed at trusts could be established which effectively created a trust arrangement on each person’s share of their joint properties. This was done by ensuring that a charge was registered against their respective shares of the property. To ensure that the shares could be charged, our clients were advised that they would have to sever the joint tenancy on their property to change the type of joint ownership to tenants in common. The sales pitch given was that by placing their property into an APT, in the event of one spouse passing away, the surviving spouse would still have the right of use of the property with the added benefit that the property would eventually pass to their intended beneficiary, being their son.

Capital Gains Tax

After agreeing to proceed, during the discussions that followed with their nominated advisor, advice was later given about Capital Gains Tax (“CGT”) and the effect that placing a charge would have on their property should they choose to sell this in the future. Our clients were advised that no charge to CGT would arise.

Our clients prepared and signed their respective APT’s and appointed each other and the directors of UW as the trustees of their respective trusts. To ensure their half shares in their joint property was charged to the trust, they proceeded with a severance of the joint tenancy and shortly thereafter signed a legal charge prepared by UW which was registered at the Land Registry against their joint property.

Reviewing the trusts

In October 2018 our clients became aware by chance of issues with UW and that the company director had been prosecuted for misappropriating funds that clients of theirs has placed into trust with UW. Our clients undertook a review of the trusts and became concerned that their property may be at risk. In addition, the wording of the legal charge was reviewed. It was discovered that due to the way in which the charge had been worded, once their property was sold, all the sale proceeds would be transferred into their respective APT’s. Further, as the charge itself was silent to the base value of the property, for CGT purposes, on sale, CGT would be paid on the full sale price. As the value of our client’s home was just short of £570,000, this would result in a significant charge to CGT being paid.

The court application

We were approached to assist with a Court application to have the charge set aside on the basis that there had been a fundamental misunderstanding about whether CGT applied. As this was not a contested application, a claim was issued at the Royal Courts of Justice in London.

A disposal hearing was scheduled in February 2020. In short, Deputy Master Nurse agreed with our application and considered that our clients had received poor tax advice from UW. Further that the effect of this did create unforeseen adverse CGT liability for our clients which was no part of what they agreed to at the time of entering into the trust arrangements. As such, he ordered that the charge registered against our client’s property should be set aside. In addition, the title to the property was to be rectified at the Land Registry.

The case is a reported judgement, which was handed down on 24 February 2020. You can access the full judgement here.

Watch previous client of Universal Wealth, Roger Wade, explain his story.